Required Minimum Distributions (RMDs)

| IRAs including SEP, SIMPLE and SARSEP IRAs | Defined Contribution Plans (e.g. 401(k), profit-sharing, and 403(b) plans) |

|---|---|

When do I take my first Required Minimum Distribution (the required beginning date)?

| You must take your first RMD by April 1 of the year following the year in which you turn 72, regardless of whether you are still employed. See Example #1, below. | April 1 of the year following the later of the year you turn 72 or the year you retire (if allowed by your plan). If you are a 5% owner, you must start RMDs by April 1 of the year following the year you turn 72. |

|---|---|

What is the deadline for taking subsequent RMDs after the first RMD?

| After the first RMD, you must take subsequent RMDs by December 31 of each year beginning with the calendar year containing your required beginning date. See Example #2, next page. | Same as IRA rule. |

|---|---|

How do I calculate my Required Minimum Distribution?

|

Your Required Minimum Distribution is generally determined by dividing the adjusted market value of your IRAs as of December 31 of the preceding year by the distribution period that corresponds with your age in the Uniform Lifetime Table. See Uniform Lifetime Table, next column, and Joint Life and Last Survivor Expectancy Table, later. If your spouse is your sole beneficiary and is more than 10 years younger than you, you will use the Joint Life and Last Survivor Expectancy Table. |

Same as IRA rule. Your plan sponsor/administrator should calculate the RMD for you. |

|---|---|

Example #1: Your 72nd birthday was June 30, 2021. You must take your first RMD (for 2021) by April 1, 2022.

| IRAs including SEP, SIMPLE and SARSEP IRAs | Defined Contribution Plans |

|---|---|

How should I take my Required Minimum Distributions (RMDs) if I have multiple accounts?

| If you have more than one IRA, you must calculate the RMD for each IRA separately each year. However, you may aggregate your RMD amounts for all of your IRAs and withdraw the total from one IRA or a portion from each of your IRAs. You do not have to take a separate RMD from each IRA. |

If you have more than one defined contribution plan, you must calculate and satisfy your RMDs separately for each plan and withdraw that amount from that plan. Exception:If you have more than one 403(b) tax-sheltered annuity account, you can total the RMDs and then take them from any one (or more) of the taxsheltered annuities. |

|---|---|

May I withdraw more than the Required Minimum Distribution?

| Yes, an IRA owner can always withdraw more than the RMD. You cannot apply excess withdrawals toward future years’ RMDs. | Same as IRA rule. |

|---|---|

May I take more than one withdrawal in a year to meet my Required Minimum Distribution?

| You may withdraw your annual RMD in any number of distributions throughout the year, as long as you withdraw the total annual minimum amount by December 31 (or April 1 if it is for your first RMD). | Same as IRA rule. |

|---|---|

What happens if I do not take the RMD?

| If the distributions to you in any year are less than the RMD for that year, you are subject to an additional tax equal to 50% of the undistributed RMD. | Same as IRA rule. |

|---|---|

Example #2: You turn 72 on July 15, 2021. You must take your first RMD, for 2021, by April 1, 2022. You must take your second RMD, for 2022, by December 31, 2022 and your third RMD, for 2023, by December 31, 2023.

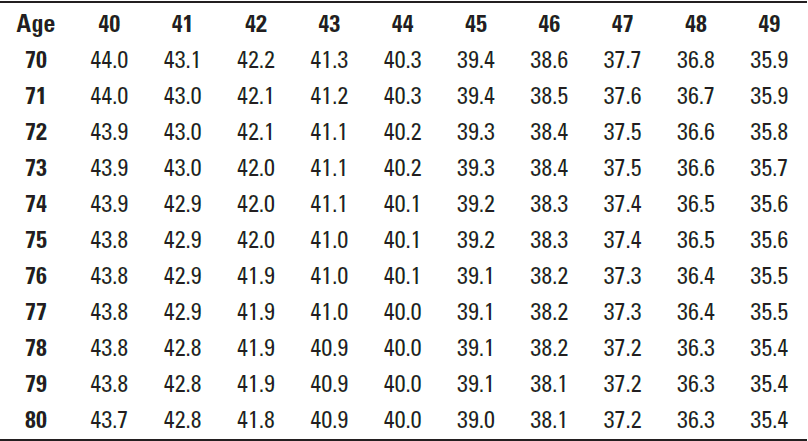

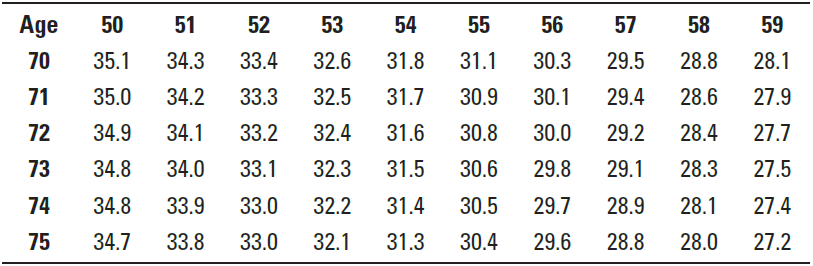

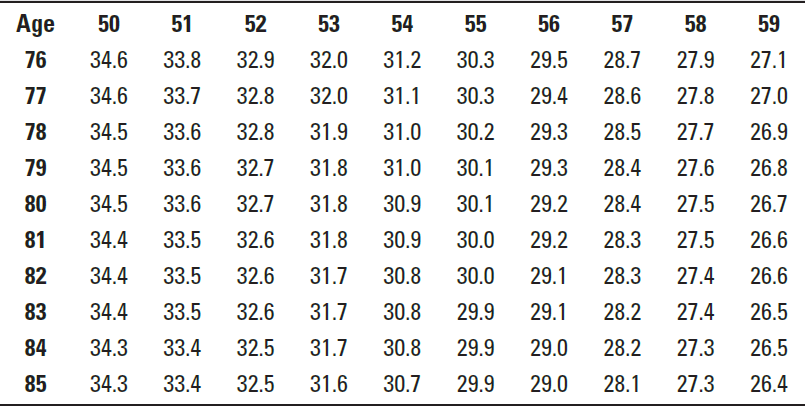

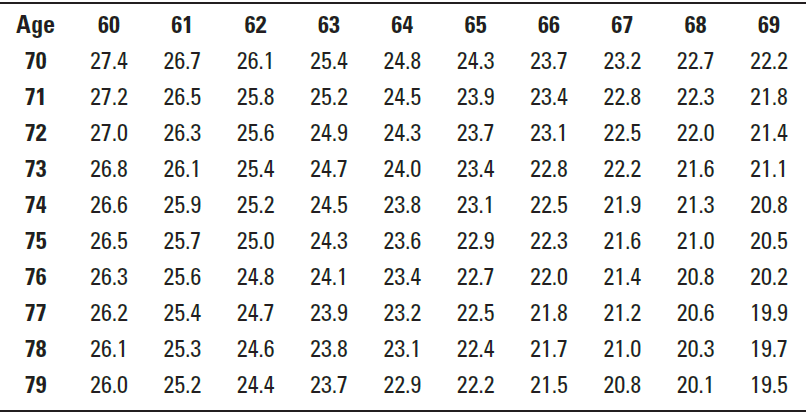

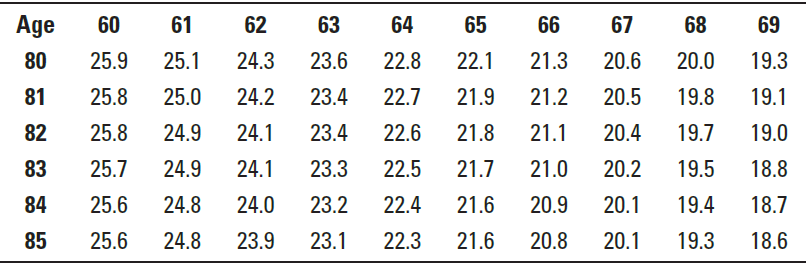

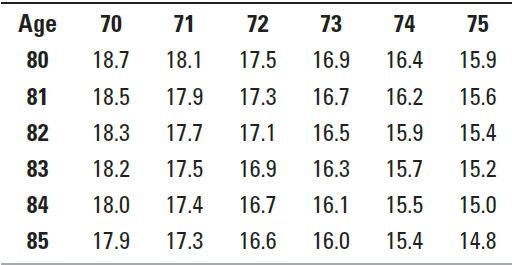

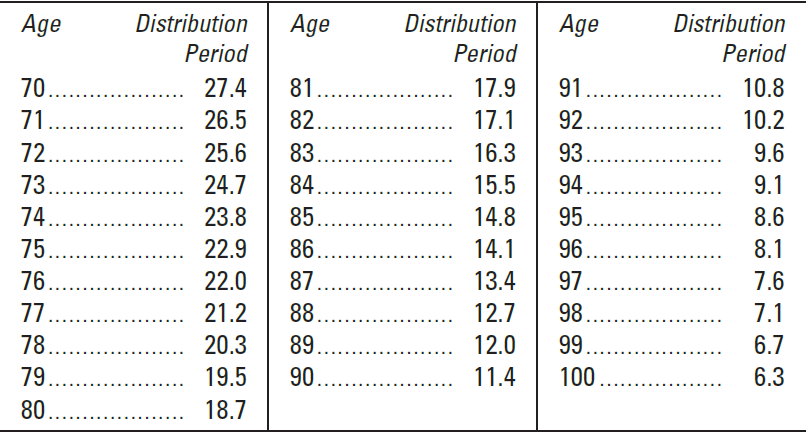

Uniform Lifetime Table

Use for unmarried participants, married participants whose spouses are not more than 10 years younger, and married participants whose spouses are not the sole beneficiaries of their IRAs. Use actual age of participant on his or her birthday for each year.

For ages not listed in this table, see IRS Pub. 590-B for the complete table.

Joint Life and Last Survivor Expectancy Table

Use for participants whose spouses are more than 10 years younger and are the sole beneficiaries of their IRAs. Use actual age of participant and spouse on their birthdays for each year.