Small Business Health Care Tax Credit

Do You Qualify?

The three steps (next column) assist small employers (business or tax-exempt) that provide qualified health insurance coverage to employees determine if they may qualify for the Small Business Health Care Tax Credit. In general, health insurance must be purchased through a Small Business Health Options Program (SHOP) marketplace.

Employees

The Small Business Health Care Tax Credit is reduced if the employer had more than 10 full time equivalent employees (FTEs) for the tax year. If the employer had more than 25 FTEs for the tax year, the credit is reduced to zero. Generally, all employees who perform services during the year are taken into account when determining FTEs.

Excluded Employees

Hours, wages, and premiums paid for excluded employees are not counted when figuring this credit. Excluded employees include the owner of a sole proprietorship, partner in a partnership, shareholder who owns more than 2% of an S corporation, shareholder who owns more than 5% of a C corporation, person who owns more than 5% of the capital or profits of any other business that is not a corporation, and family members or a member of the household who qualifies as a dependent of any person listed above.

Seasonal Employees

Seasonal employees who work 120 or fewer days during the tax year are not considered employees in determining FTEs and average annual wages. But, premiums paid on their behalf are counted. Seasonal workers include retail workers employed exclusively during the holiday seasons.

Do You Qualify?

1) Does the employer pay at least 50% of the employee insurance premiums at the single (employee-only) coverage rate?

If yes, continue to Step 2. If no, stop here. You do not qualify for the credit.

2) Determine the total number of employees (not counting owners or family members).

Full-time employees _________

(Enter number of employees that work at least 40 hours per week.)

plus

Full-time equivalent employees _________

(Calculate the number of full-time equivalents by dividing total annual hours of part-time employees by 2,080.)

equals

Total employees _________

If the total number of employees is less than 25, continue to Step 3. If no, stop here. You do not qualify for the credit.

3) Calculate the average annual wages of employees (not counting owners or family members).

Total annual wages (Medicare wages) paid to employees _________

divide by

Number of total employees from Step 2 _________

equals

Average wages * _________

* If the result is less than $56,000 (2021), the employer may qualify for the Small Business Health Care Tax Credit.

Full-Time Equivalent Employees (FTEs)

The employer’s number of FTEs is determined by dividing the total hours of service for which the employer pays wages to employees during the year (but not more than 2,080 hours for any employee) by 2,080.

Average Annual Wages

The Small Business Health Care Tax Credit is reduced if the employer paid average annual wages of more than $27,000 for the tax year. If the employer paid average annual wages of $56,000 or more for the tax year, the credit is zero. Wages, for this purpose, mean wages subject to Social Security and Medicare tax withholding determined without considering any wage base limit. Average annual wages are total wages paid for the tax year divided by the number of FTEs.

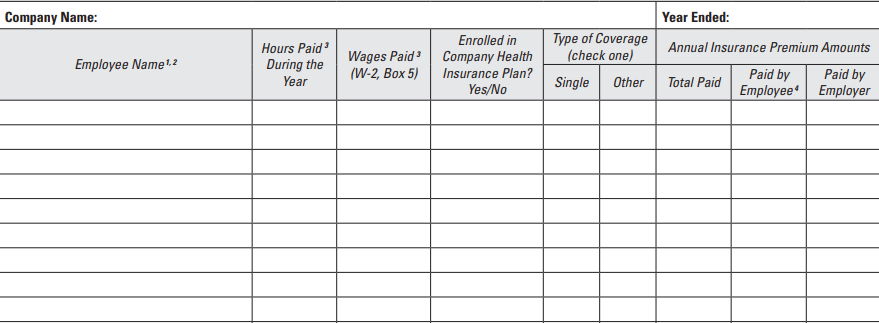

- Do not list any owner or owner’s family members.

- Indicate any seasonal employee who worked 120 or fewer days during the tax year.

- Do not include hours worked or wages paid to seasonal employees. Do include premiums.

- Employee paid premiums include any premiums paid pursuant to a salary reduction plan under a IRC section 125 cafeteria plan.